Given the market volatility of the past 15 years, with both the “tech wreck” and the financial crisis, a growing number of consumers are seeking more safety for their investment portfolios, through everything from more proactive risk management strategies, to using products like equity-indexed annuities and structured notes that explicitly provide for "some" upside participation in bull markets, but with downside protection in a bear market.

Yet the reality is that constructing downside protection and a principal guarantee over time doesn’t actually require products like equity-indexed annuities and structured notes. They can actually be constructed with relatively simple combinations of bonds and either stocks or equity index options. In fact, just buying a portfolio of bonds and using the interest to buy at-the-money call options is sufficient to produce a partial upside participation rate in equities with a downside guarantee!

Unfortunately, though, creating such pairings can be especially difficult in low interest rate environments, as there simply isn’t enough yield to afford very many options contracts, which in turn results in relatively low equity participation rates. Yet given that annuity companies and structured note providers are subject to the same constraints, in the end investors will likely suffer from low returns in such solutions, regardless of which vehicle is used… and in fact may have the greatest upside potential by simply constructing the strategies themselves, and avoiding the internal costs of such products in the first place!

Structured Note Alternatives - Building A 10-Year Downside Guarantee For Stocks Using Government Bonds

Structured Note Alternatives - Building A 10-Year Downside Guarantee For Stocks Using Government Bonds

Imagine for a moment that you wanted to invest in equities for the next 10 years, but have a guarantee that there would be no downside risk; no matter what, you want to be assured that the portfolio will return at least your principal at the end of the decade.

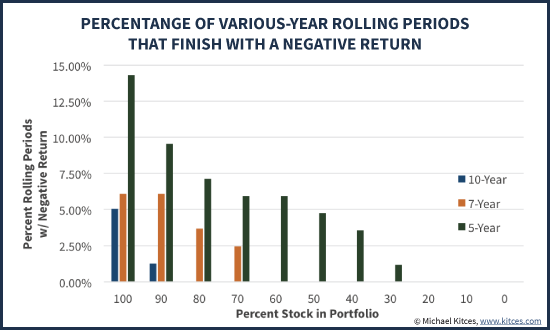

On the one hand, an investor could simply approach this by recognizing that the probability of having a (nominal) loss in equities over a decade is already a very low probability event, and one whose probability declines even further by diversifying into bonds. The chart below shows the probability of having a cumulative total return that is negative after rolling 5-, 7-, and 10-year periods, for portfolios varying from 100% in stocks in 100% in (intermediate term government) bonds.

Not surprisingly, while the odds of a negative return are fairly low across the board, and the odds decline further as the time horizon lengthens and the portfolio becomes more conservative. While many portfolios may still be negative after 5 years, historically over a 7-year time period, a portfolio with 60%-or-less in stocks has never had a negative cumulative return. Over a 10-year time horizon, as long as bond exposure is at least 20% (i.e., equity exposure is down to 80%), a negative cumulative return has never occurred over such a "long" time horizon; in other words, to the extent that equities were down at all, with as little as 20% in bonds the bond return was enough to fully offset any losses.

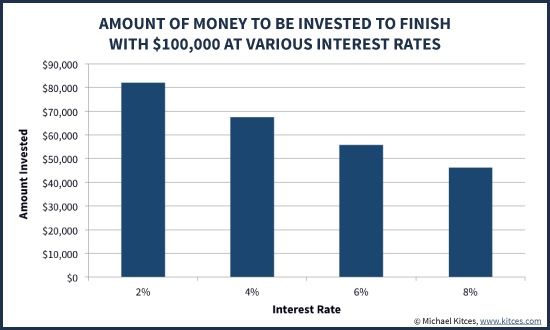

Of course, while equities have historically always recovered enough that 20% in bonds is "enough" over a 10-year time horizon, in the extreme an investor could actually guarantee that the portfolio will never have a negative return, simply by buying enough 10-year government bonds to ensure that just holding until maturity alone will replenish the entire principal. In such a scenario, even if the stock market in the aggregate went to zero, the bonds alone would still mature with sufficient value to replenish the original principal. Of course, the amount it takes in bonds to provide for that principal replacement depends on the (10-year) bond yield in the first place; the higher the yield, the less it takes in bonds to replace the principal down the road (and the more than can be invested into equities), while in today’s environment with lower yields, it takes far more, as shown in the chart below. (Chart assumes the investor simply buys 10-year zero-coupon Treasury STRIPS at the specified rate.)

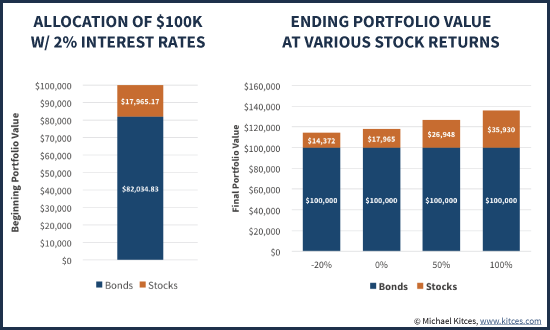

Once Treasuries are in place to secure the “floor”, the investor would simply put the rest of his/her funds into equities… at a 2% interest rate, this would require about 82% of the portfolio in bonds, and the remaining 18% in equities. As noted earlier, in this scenario the stocks could go all the way to zero, and the investor would still be protected because the bonds alone would mature at par to replace the original ($100,000) portfolio value.

In fact, even if equities were merely flat for the decade, the investor would still end out with 100% of the original principal (from bonds), plus 100% of the original investment in equities, resulting in a final value up 18% cumulatively, for a modest positive total return of about 1.67%/year. Even if equities are down 20%, there will still be a positive return for the total portfolio of about 1.35%/year! And of course if equities are up, the investor just makes even more on top of the bond return. Either way, the principal guarantee stays intact no matter what.

Of course, because a large portion of the funds were occupied by the bond allocation – especially given today’s low interest rates – the investor only gets a “modest” participation in the total upside of equities. Even in the scenario where the market grows by 100% cumulatively in a decade (an average annual growth rate of about 7% for the stocks), the overall portfolio is only up at a 3.1% average annual compound growth rate. In other words, the investor only participated in about 44% of the total upside in this bull market scenario. But then again, the investor got that upside participation with no downside risk at all, as principal itself was entirely secured by just the bonds alone. Given current Treasury yields, any investor could theoretically do this today.

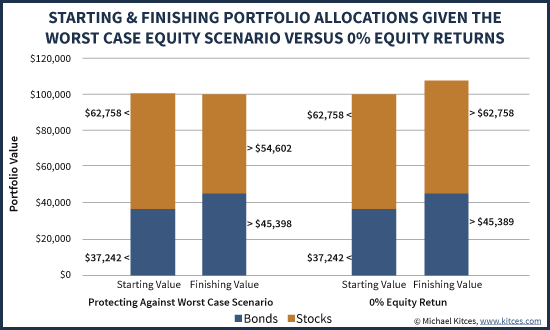

Notably, one of the caveats to the strategy of pairing Treasuries-to-replace-principal with a stock allocation is that even if stocks finish flat, the portfolio will technically be up. In order to achieve a scenario where the total return is zero when stocks are flat, the investor could choose to allocate less to bonds and more to stocks - for instance, putting in enough that even if stocks do have their worst decade ever, the remaining value in equities - plus the value of the bonds - would be enough to replace/secure the original $100,000 portfolio value. And if the equities "merely" finished flat (at a 0% return), the portfolio again would be up at least a little.

Pairing Treasury Bonds With Equity Index Options For A More Efficient Downside Guarantee

Given the challenges of cleanly aligning a guaranteed floor and equity upside by pairing together stocks and bonds directly, an alternative way to structure the transaction is to use bonds and equity index options, as the latter provide for a more effective “alignment” of upside and floor guarantee.

Given the challenges of cleanly aligning a guaranteed floor and equity upside by pairing together stocks and bonds directly, an alternative way to structure the transaction is to use bonds and equity index options, as the latter provide for a more effective “alignment” of upside and floor guarantee.

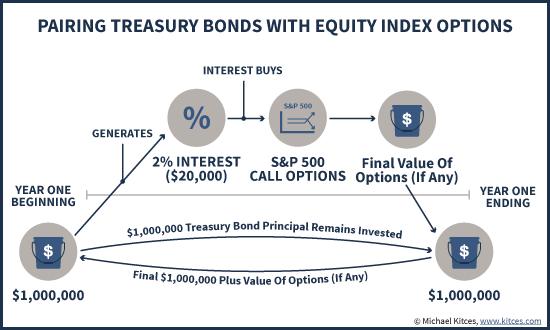

For instance, in the simplest scenario, an investor might simply buy a series of 10-year Treasury bonds, and use the annual bond interest to buy a series of 1-year at-the-money call options for the desired equity index (e.g., the S&P 500). At worst, if the market doesn’t go up for 10 years, the options will expire worthless every year, but the bonds remain to mature at par at the end of the decade, returning the target principal amount. And any year the options expire inthe money, the investor participates in (at least some of) the upside.

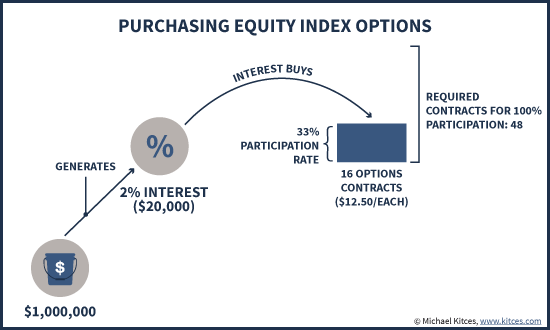

Of course, at today’s low interest rates, there’s not a lot of interest available to invest into those options. With the 10-year Treasury yielding roughly 2%, and an at-the-money call option on SPY available for $12.50 for a strike price of $210 (as of when the S&P 500 was at 2,100), an investor with a $1,000,000 portfolio could buy roughly 16 options contracts (with the 2% x $1,000,000 principal = $20,000/year of interest). Of course, it would actually take about 48 call options at a strike price of $210 to get full equity participation on a $1,000,000 account, so buying “just” 16 options contracts would give the investor an upside equity participation rate of roughly 33%.

In other words, given what today’s interest rates will bear out in buying call options, the investor effectively gets a 33% participation in the upside price movement of the S&P 500 (note: price changes only, as options don’t pay dividends!), with “no downside”, since at worst the options merely expire worthless at the end of the year and the investor buys new options again next year while bond principal remains intact (to mature at par at the end).

Since options would be purchased one year at a time in this example, each year the starting point for equity participation will “reset” to the then-current level of the index, and the participation rate itself will fluctuate up and down with then-current pricing of options (which may be more or less expensive, depending on changes in volatility along the way).

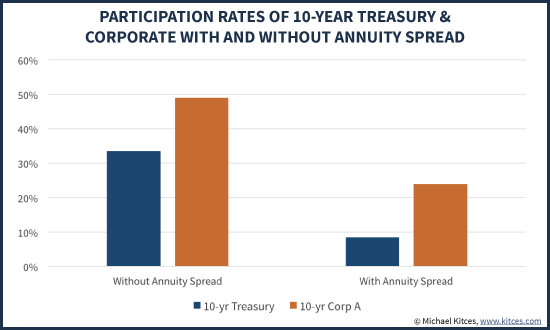

Of course, to the extent that the investor is comfortable taking a little more risk, the participation rate can be improved further. For instance, with 10-year A-rated corporate bonds (slightly greater risk of default than Treasuries) yielding approximately 2.9%, using that interest buys enough options contracts to produce a first-year participation rate of 49% instead of “just” 33%.

On the other hand, the caveat is that in the context of an equity-indexed annuity (or a structured note that functions in a similar manner), participation rates will be lower, as the insurance company needs an opportunity to make money as well, as a for-profit entity (not to mention recovering its costs of overhead and distribution). With an equity-indexed annuity, this is accomplished through an interest rate spread – in other words, while the insurance company might invest in bonds that pay 2%, it may keep 1.5% of that interest yield to cover everything from overhead to profit margins to the commissions paid to the selling agent, with only the remaining 0.5% yield going into options. Given today’s low interest rates, though, cutting out a 1.5% interest rate spread has a dramatic impact, reducing the participation rate to only 8% using 10-year Treasuries and 24% with a 10-year A-rated corporate bond.

Because the participation rate is driven by the number of options contracts purchased, and the free cash flow to purchase those options is derived from bond interest, the overall level of interest rates turns out to be a key factor in the potential participation rate of an equity-upside-with-downside-protection strategy. If/when/as interest rates rise, so too will available participation rates, either for equity-indexed annuities, structured notes, or for investors and advisors who wish to construct their own using bonds and options.

On the other hand, as long as interest rates stay low, both insurance companies and investors may feel forced to find other means to boost participation rates, either through strategies to increase the yield and available dollars to buy options, or to manage the (net) cost of options.

For instance, an investor might own different (e.g., lesser quality) bonds to stretch for greater yield, or move into other segments of the bond market that might otherwise generate better cash flows. The more the bond cash flows, the more money there is to buy options, and the greater the upside participation rate. In the context of equity-indexed annuities, insurance companies often use their size and scale to negotiate for better pricing on bond deals to maximize their yield. Investors can also boost their participation rates by giving up a bit on their guarantees in the first place; for instance, if guaranteeing “just” 90% of the principal is sufficient, the investor can put less money in bonds, which frees up more capital to invest over time towards options instead, resulting in more equity upside participation.

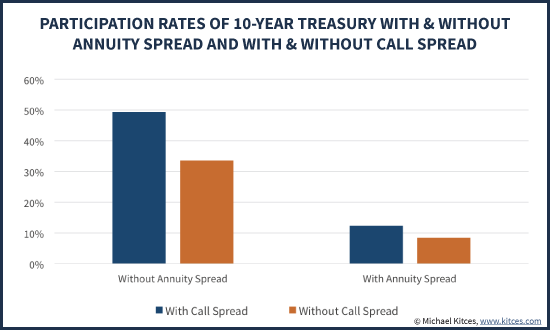

Alternatively, the net cost of options can also be reduced with call spreads, like buying an at-the-money option but selling an out-of-the-money call option at a higher strike price. The net result puts an effective cap on the maximum appreciation, but increases the participation rate along with it. For instance, a call option for SPY at a strike price of 230 costs approximately $4.00 (at the time of this writing when the S&P 500 is around 2,100), which would reduce the net cost of an at-the-money call option from $12.50 to only $8.50. In turn, this would allow a larger number of options to be purchased, but the maximum appreciation for the year would be limited to only about 9.5% (the gain from 210 to 230 on the SPY, corresponding to 2,100 to 2,300 on the S&P 500). Of course, when purchased from an equity-indexed annuity company (or a structured note) that must charge an annuity interest rate spread, participation rates will still be compressed slightly.

Amplifying Participation Rates In A Low Yield World With Call Spread Caps And Monthly Averaging

Notably, in the context of equity-indexed annuities in particular, insurance companies have also sought to increase participation rates by shifting from annual point-to-point strategies (i.e., participation in the one-year price return of an index like the S&P 500) to “monthly averaging” strategies instead. With monthly averaging, the investor’s return is calculated by taking theaverage price of the index throughout the year, comparing it to the original, and calculating the appreciation accordingly. Thus, for instance, if the market went up 12% for the year by rising 1% each month, the S&P 500 would grow from 2,100 to approximately 2,350, and the averageprice for the year would be about 2,225. Since 2,225 is a 6% increase over the starting level of 2,100, the monthly averaging formula would return 6%, then further adjusted by the participation rate (so if the participation rate was 75%, the final return would be 6% x 75% = 4.5%, even though the market was up 12% overall).

Notably, in the context of equity-indexed annuities in particular, insurance companies have also sought to increase participation rates by shifting from annual point-to-point strategies (i.e., participation in the one-year price return of an index like the S&P 500) to “monthly averaging” strategies instead. With monthly averaging, the investor’s return is calculated by taking theaverage price of the index throughout the year, comparing it to the original, and calculating the appreciation accordingly. Thus, for instance, if the market went up 12% for the year by rising 1% each month, the S&P 500 would grow from 2,100 to approximately 2,350, and the averageprice for the year would be about 2,225. Since 2,225 is a 6% increase over the starting level of 2,100, the monthly averaging formula would return 6%, then further adjusted by the participation rate (so if the participation rate was 75%, the final return would be 6% x 75% = 4.5%, even though the market was up 12% overall).

Ultimately, monthly averaging formulas will (on average) produce lower returns in bull markets than point-to-point structures since markets average positive returns (e.g., a normal point-to-point one-year option in this example would have applied the participation rate to 12% upside instead of only 6%). However, because the monthly averaging options contracts are generally cheaper (for this same reason about their expected returns), annuities based on them will tend to have higher participation rates; in the end, given the different combinations of upside potential and participation rates in that upside, investors may not actually see substantively different returns either way (e.g., 75% participation on 6% appreciation in a monthly average formula is similar to getting 40% participation on the 12% upside in a point-to-point formula). In many cases, which is better will simply depend on the exact path the market takes for the year - at least, if all else is held equal (though that is not always the case).

While monthly averaging options in particular generally aren’t available to consumers (as they’re privately negotiated derivatives for insurance companies that aren’t traded on public exchanges for consumers to purchase), the remaining strategies of investing for greater bond yields, accepting diminished principal guarantees in exchange for more upside, and using call option spreads to get greater participation but with an upside cap, are all feasible for individual investors. In other words, advisors and their clients really can build their own equity-indexed annuity or structured note solutions, but without the annuity or structured note itself (though notably, this "do-it-yourself" solution also loses out on the tax-deferral treatment of annuities, which may be relevant for some clients!).

Of course, the irony of building “your own” principal guarantee is that it does mean trading in options, and watching – at least in down years – the value of those options potentially going all the way to zero. While that -100% return will by definition only be for a very small percentage of the portfolio, the fact remains that for many investors, it may actually be morepsychologically comforting to not see how the sausage is made and just view a single account balance with a floor (as occurs with equity-indexed annuities and structured notes)… although as noted earlier, the interest rate spread of an annuity (or structured note) can significantly undermine the potential upside of such “packaged” floor-with-upside investment strategies in low yield environments, so that psychological comfort has a potentially significant cost trade-off!